Analyzing a Cash Flow Statement

Understanding cash flows are essential to picking the right stock.

One of the favorite tools of Warren Buffett and late Charlie Munger.

Earnings can be subjective, but cash flow is a concrete measure. This makes the Cash Flow Statement a crucial component of a 10-K report1. I use this all the time when analyzing stocks. It helps me to know which companies generate (or burn) cash and how they generate (or burn) it.

What is a Cash Flow Statement?

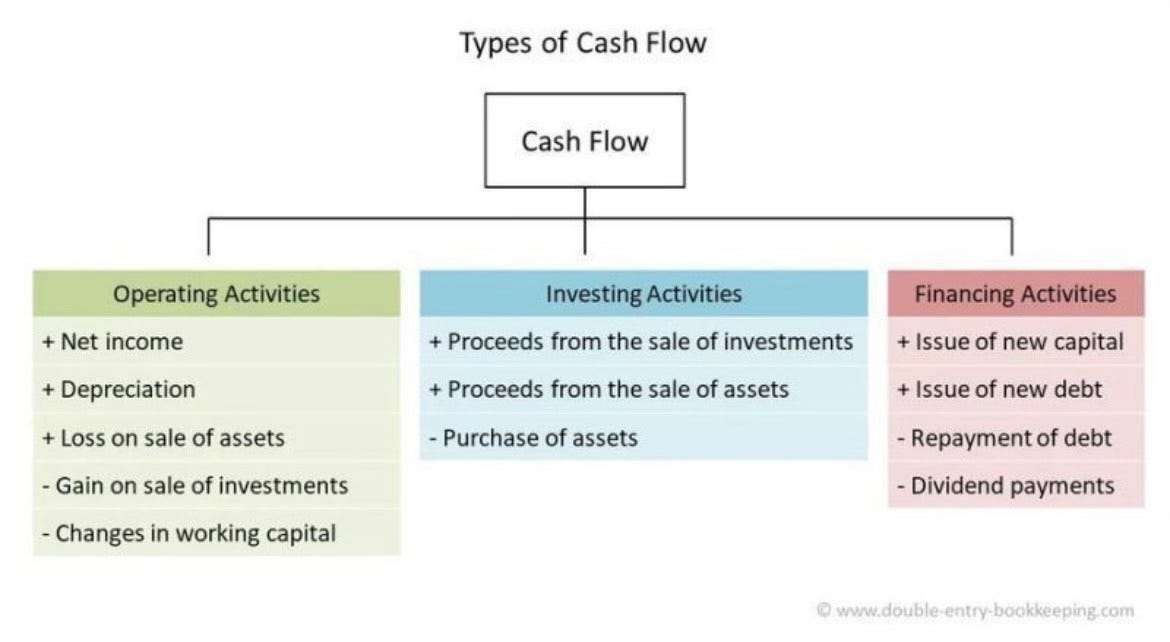

A cash flow statement details the cash inflows and outflows of a company over a specific period. Its primary purpose is to monitor the movement of cash within a business. Investors should look for companies that generate and manage cash efficiently. A typical cash flow statement has three sections: - Cash Flow from Operating Activities - Cash Flow from Investing Activities - Cash Flow from Financing Activities

Cash Flow from Operating Activities

This section shows the cash generated from a company's core business operations. In essence, it reflects the cash earned from the sale of its main products or services. For instance, if a beer company earns $2 per beer in operating cash flow and sells 2 million beers in a year, its cash flow from operating activities would be $4 million. While similar to net income, the cash flow from operating activities excludes certain income and expenses that do not involve actual cash transactions. The formula for calculating this is: Cash Flow from Operating Activities = Net Income + Non-Cash Charges +/- Changes in Working Capital

Cash Flow from Investing Activities

This section provides an overview of the company's income and expenses related to investments. Key components include: - Capital Expenditures (CAPEX) - Mergers & Acquisitions - Marketable Securities The calculation is as follows: Cash Flow from Investing Activities = Sale of Marketable Securities + Divestments - CAPEX - Mergers & Acquisitions - Purchase of Marketable Securities

Cash Flow from Financing Activities

This section measures the cash flow between the company and its shareholders and debtors. It provides insight into how the company finances its operations. Main components include: The formula is: Cash Flow from Financing Activities = Debt Issuance + Issuance of New Stocks - Dividends - Debt Repayments - Share Buybacks

Changes in Cash Balance

Finally, the total change in cash balance is calculated as: Cash at the End of the Year = Cash at the Beginning of the Year + Cash Flow from Operating Activities + Cash Flow from Investing Activities + Cash Flow from Financing Activities

I hope this has been helpful. If you have any questions or any feedback you would like to share, do write me in the comments or by direct message. 💚🙏

Your Etcaetera

Akim

10-K Report: required by the U.S. Securities and Exchange Commission, it is a report about financial performance filed annually by a publicly-traded company.