Deep Dive into Alphabet - Part 2

The hard figures and risks!

Welcome to the 2nd part of the deep dive on Alphabet (GOOG/GOOGL)! The 1st part was released by my friend and partner on this collaboration, Timothy (Panic Drop).

In this second part, we focused on Alphabet's stock performance, the bright financials, its attractive valuation, and the regulatory risk currently shadowing the stock.

Financials and Valuation of Alphabet Inc.

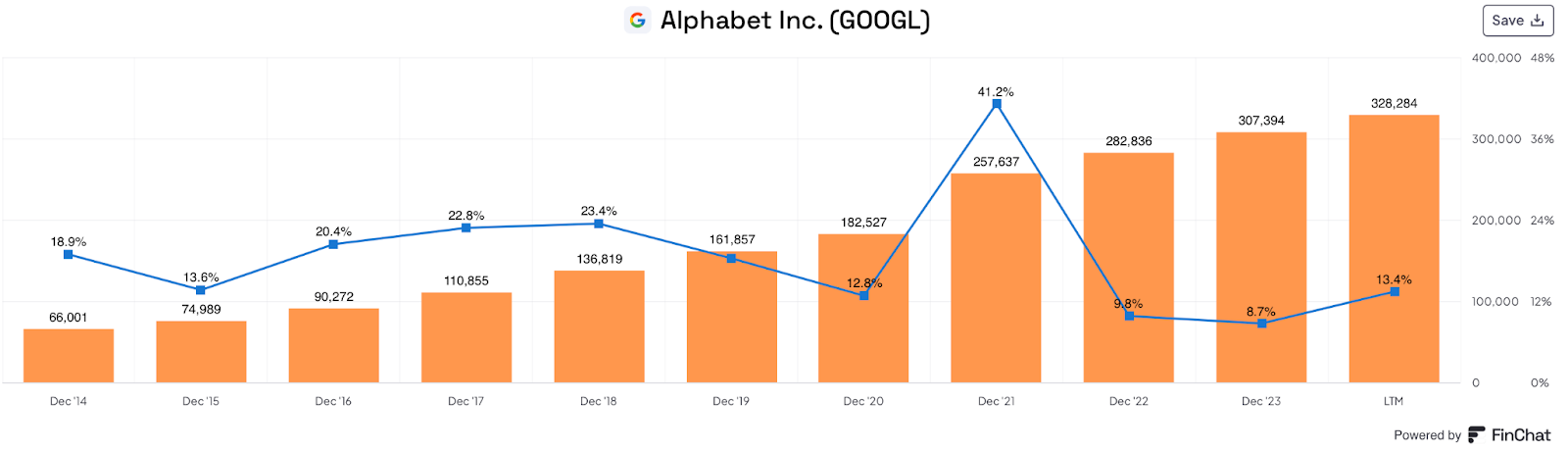

Alphabet’s growth has been truly exceptional. It is one of the few stocks with double digit growth rates for 8 years in a row in the last decade! The company has had an average revenue growth of 19% per year in the period 2014-2023.

There’s been a slowdown in 2022 and 2023. And this caused a rough stock price slump amidst an already difficult stock market, causing the stock to lose 30% of its value within a few months.

There is a double reason for that revenue growth slowdown: first is the 2021 base year effect with an extraordinary 41.2% revenue growth rate. This naturally caused the couple of years after to have a slower than average growth rate.

The second reason for the revenue growth slowdown is actually a temporary growth break (so to speak) the CEO Sundar Pichai and his management took to 1. invest massively in AI (which affects the revenue growth temporarily) and 2. increase the business efficiency. Indeed, both ROE and ROA hit record levels in 2022 and 2023.

The CEO performed an “efficiency reset” and we start seeing the results today. We are noticing a reacceleration in the growth which potentially opens the door to a return to the 19% average growth rate or above, in case of AI and Cloud advancements as described in Timothy’s first part.

LTM key figures:

ROA of 22.0% and ROE of 30.9%, the highest ratios in the last decade (except for 2021)

Gross profit margin of 57.6% and FCF of 18.5%

$1.8 mn revenue per employee (highest in a decade, matched only by 2021 revenue per employee)

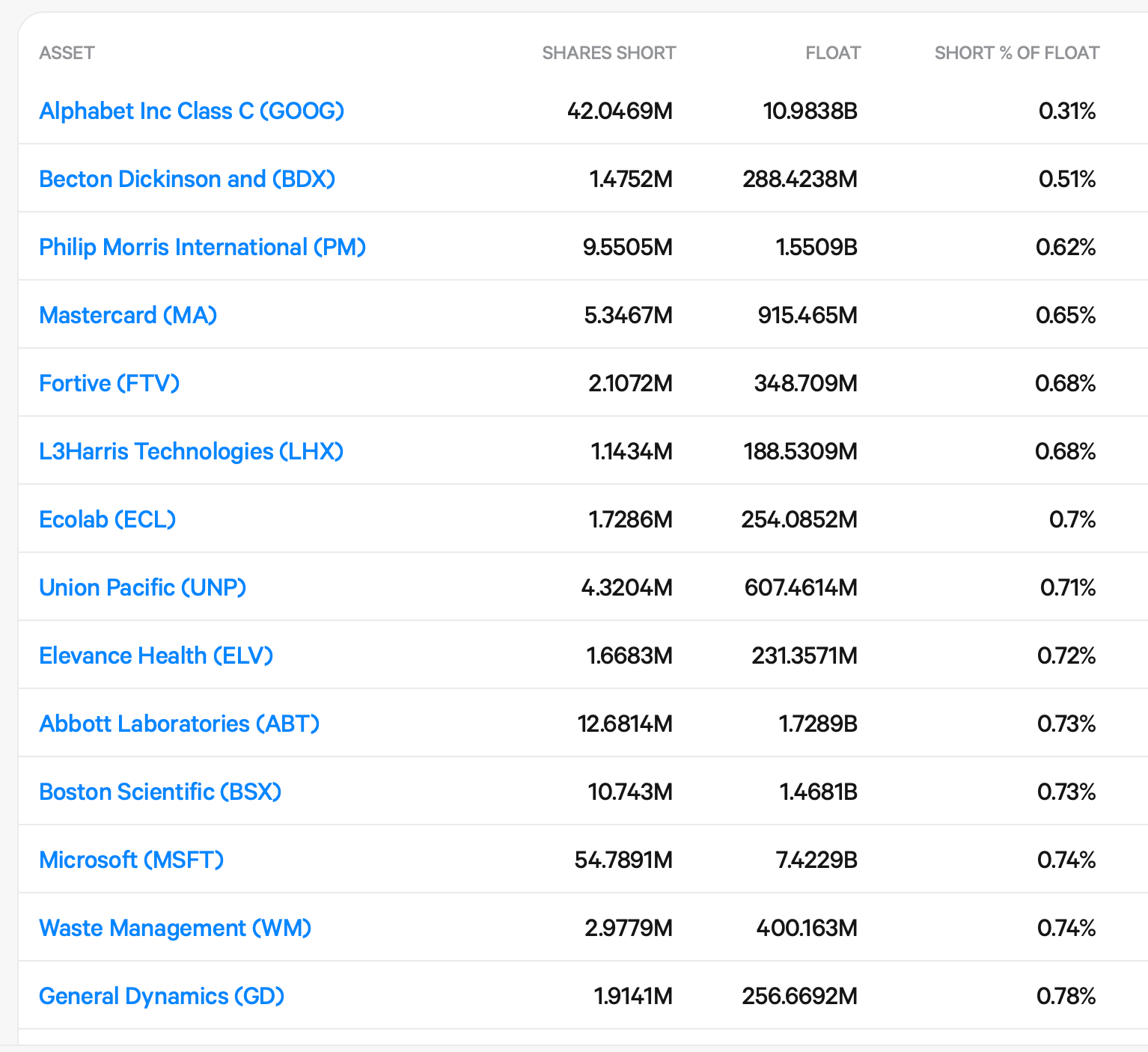

Quite logically, when you have such an impressive financial health, the shorters will stay away from the stock. As a matter of fact, it is the least shorted stock in the S&P 500, less shorted than stocks like Microsoft even!

Despite the low short interest, the stock is far from trading at an expensive level. Actually, it is the cheapest stock among the Mag-7 stocks in terms of price to earnings. Also when considering its own historical valuation, the stock is looking pretty cheap.

Alphabet is trading at 22.5x LTM earnings and 19.8x NTM earnings, clearly on the very lower end of the decade-long range. The stock has frequently traded around or above 30x LTM earnings, indicating at least 30% upside, which would put it a little above $200 per share. Interestingly, that is also where lies the average price target of the Street ($202). The main reason the stock is currently trading for cheap is its current principal fear factor, the regulatory one.

Regulatory Risk Factor

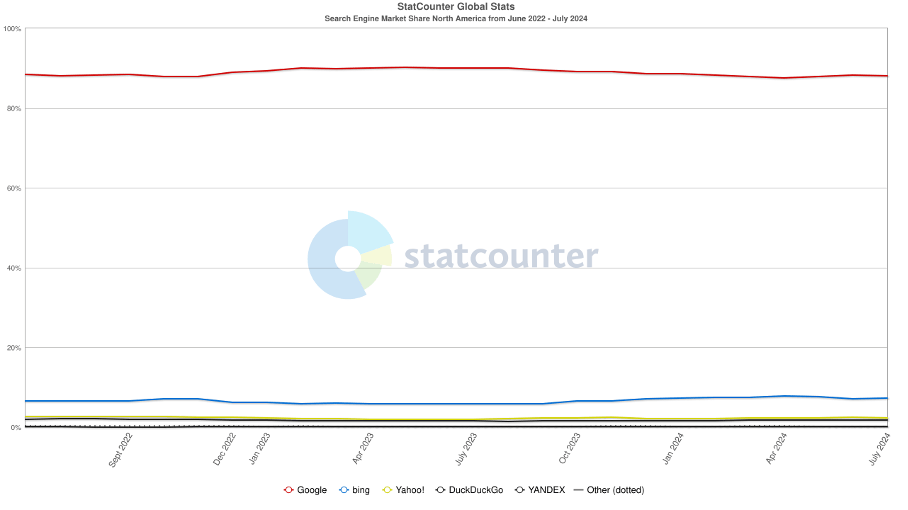

Alphabet (and Google in particular) is often subjected to enhanced scrutiny (and fines) in multiple jurisdictions. This more of a luxury than anything else, because it shows the importance that the business has gained in the data segment with a fairly constant 90% market share despite high competition.

But these fines and other lawsuits have been fairly immaterial, given the cash that the company generates. The major risk that causes shareholders to tremble in recent weeks is an antitrust suit by a U.S. District Court that says Google violated Section 2 of the Sherman Act by behaving in a monopolistic manner. Alphabet allegedly used expensive agreements in order to maintain its monopolistic position as the number one search engine in the world. This could cause the regulatory bodies to require a split of Alphabet, although in our opinion this is more of a feared rumor than anything else. The U.S. needs large tech companies to stay ahead in the big data game, especially at a time where it is becoming more crucial than ever for generative AI advancements. It is also probable that the regulatory risk is already fully priced in, given how cheap the stock is trading.

The Chart

GOOG is currently testing its 200-day moving average (green), a level that has previously served as a strong level to hold. Additionally, it's trading at a 21% discount compared to its $202 valuation, indicating potential upside.

Bottom Line

Alphabet is an attractive investment opportunity and a great stock to own in a diversified portfolio. The growth rates, the increased efficiency and the relatively low valuation make the stock perhaps the most attractive of the Mag-7 - especially after the recent regulatory fears providing a discount and an excellent entry (or accumulation) opportunity. It is not for no reason that the stock is at the top of the holdings of both my portfolio (Etcaetera) and Timothy’s (Panic Drop).

Thank you for reading the second part of this deep dive on Alphabet. We hope you enjoyed it! Please remember to subscribe to both newsletters if you liked our analysis. We plan to continue doing collaborations together, this one being already our third in as many months!

Etcaetera & Panic Drop

Consider subscribing to Panic Drop as well:

| A guest post by

|